Social Security Planning for Widows: When to Start Taking Benefits

What the Widow Needs to Know to Before Making a Decision on When to Start Claiming Benefits.One of the most common questions asked by a new widow is what happens to Social Security benefits after the death of their spouse. The answer is, like so many other financial questions, it depends.

Social Security Widows Benefits: Getting Started

Table Contents

- Social Security Planning for Widows: When to Start Taking Benefits

Social Security (SS) is a complicated machine with many moving parts. The Social Security Administration’s (SSA) Program Operations Manual System (POMS) has over 20,000 pages! This first section will focus on the basics of a surviving spouse’s Social Security benefits. The sections below will go into more detail and cover specific situations dealing with young widows, spouses with age differences, ex-spouses, multiple marriages, the impact of government pensions and the logistics of applying for benefits. There’s much to cover, so let’s get started.

Note: The SS benefits discussion in this blog covers common situations. Complicated or rare situations do occur and may affect your eligibility and SS benefit claiming strategies. It is always recommended that you contact the SSA with your specific details.

When Should a Widow Start Collecting Social Security?

Please read the next sentence very carefully. Do not apply for any SS benefit without first analyzing your situation to know which claiming strategy makes the most sense for you!

Choosing the wrong SS claiming strategy may cost you hundreds of thousands of dollars over your lifetime! Of the top 25 online checklists for widows, only one mentioned SS claiming strategies. The other 24 checklists simply directed the reader to contact the SSA and apply for benefits! What’s wrong with that you say? Time and time again we find that representatives at the SS office either don’t understand the various claiming strategies or they tell you they can’t offer advice on which SS benefits to claim and when to claim them.

Picking the wrong benefit at the wrong time could cost the unaware widow many, many thousands of dollars over her lifetime. If you have options, you need to know the financial impact of choosing one option over another. Many of those 25 online checklists are provided by financial advisors which may mean they don’t understand how SS works for widows and can’t come up with a beneficial SS claiming strategy for you. This is worrisome to me and it should be to you too.

How to get started:

1. Obtain Your SS Benefit Statement

It’s always good to have and review a recent copy of your own SS benefit statement. Starting at age 60 and up to the point you start benefits, the SSA will mail a paper benefit statement to you about three months prior to your birthday. If you are under age 60 or can’t find your paper statement, you can get your benefit statement online. If you have started SS benefits, you will no longer receive the standard 4-page green and black statement but should receive a letter outlining changes to your benefits for the upcoming year.

If you don’t already have an online account with the SSA, go to www.ssa.gov. Click the Sign In/Up link at the upper right corner, then click the my Social Security box on the left and half way down the next page click Create an Account. There are a few more steps required to establish your account. When logging in to your established account, you will need to enter an 8-digit security code texted to your cellphone. Agree to the Terms of Service and your next page is the Overview where you access your full benefit statement. I suggest not getting the estimated benefits but go a little further down the page to Print / Save Your Full Statement.

2. Your Spouse’s SS Benefit Statement

Unfortunately, you cannot obtain your deceased spouse’s benefit statement online. If your spouse was at least age 60, they might have received their benefit statement in the mail.

If the SSA was already notified of your spouse’s passing, your spouse’s online account is no longer accessible. Also, you can’t register for or sign in to your spouse’s online account as it is not allowed by the SSA. As a widow, to obtain your spouse’s SS benefit information, you will need to visit a local Social Security office and take the required documents:

- your certified birth certificate,

- SS card

- marriage license

- your spouse’s SS card

- certified birth certificate

- death certificate

There may be other documents required depending on your situation such as military discharge papers (DD Form 214) and citizenship papers. If young children are involved, you’ll need their SS cards and certified birth certificates. If an ex-spouse died, you’ll need their SS number, birth certificate and death certificate as well as information on other past spouses or current spouse of your deceased ex-spouse.

Checking SS Earnings History

One reason you want your (and your spouse’s) Full Statement is to check earnings history on file with the SSA. The graphic below shows the top of the third page which contains every year you worked and how much of your earnings was taxed for Social Security and for Medicare (this does not represent your benefit, so please don’t use the displayed numbers and amounts for your own benefit analysis). Mistakes have been made in the past and sometimes one or more years of earnings is misreported which can affect your benefit amount. The Full Statement includes instructions to report corrections to your work history.

How to Read the Benefit Information on Your SS Statement

Below is a sample of the top of the second page of a SS Benefits Statement (this does not represent your benefit, so please don’t use the displayed numbers and amounts for your own benefit analysis). The first thing to note on the very top is the word “Estimated”!

Not until one applies for benefits or meets with an SSA representative, will they know exactly how much they can collect. The estimated benefits below are based on continuing to work and earn the current wage amount until the age mentioned in that row of information.

For example, if the person below stops working prior to age 67 or makes less than expected, and starts their SS benefit at age 67, the amount received will mostly likely be less than the $2,820 a month shown here. The second amount shows $3,584/month, and this is the estimated amount if this person works until age 70 and then starts collecting their own retirement benefit. The third amount of $1,893 a month is received if this person works until age 62 and starts collecting their own retirement benefit at that time.

The SS retirement benefit is a person’s own benefit which is different from a survivor’s benefit and different from a spousal benefit. If you are reading your own SS benefit statement, it will not show any surviving spouse/widow or spousal benefit numbers for you. Surviving spouse/widow and spousal benefit amounts, for you, are derived from your spouse’s SS benefit statement.

The graphic below includes a Family Survivor’s section which will be covered below discussing SS benefits for widows who are raising young or disabled children of the deceased spouse.

Common Social Security Terms

Let’s review a few common Social Security terms so that all of us are using the same terms in the same way. The SS timeline is important too and we will look at the various ages and how they impact your SS benefits.

Retirement Benefit – Is the SS retirement benefit earned by you based on your wages over your lifetime. This is what most people think of when they say they are collecting Social Security. In SSA lingo this benefit is referred to as a Retirement Insurance Benefit (RIB).

Spousal Benefit – Is the SS benefit you qualify for based on your spouse’s wages earned during their lifetime. If you also worked, you may have your own Retirement Benefit, and if you are married, you may also have access to a Spousal Benefit (but you can’t collect your full retirement and full spousal benefits at the same time; they don’t get added together for a benefit larger than either one of them). In SSA lingo this benefit is referred to as a Spouse’s Insurance Benefit (SIB).

Survivor Benefit – Is the SS benefit you qualify for based on your spouse’s wages earned during their lifetime and due to their death. Based on your spouse’s earnings, you may be able to collect a spousal benefit while they are alive or a survivor benefit if they are deceased. You can’t collect both a spousal and survivor benefit at the same time. In SSA lingo this benefit is referred to as a Widow(er)’s Insurance Benefit (WIB).

Children’s Benefit – is the SS benefit a child can receive not only if they are disabled, but if their parent is disabled, retired or deceased. Even a grandchild raised by their grandparent may qualify for a Children’s Benefit. Age, marital and dependent status and employment limits apply.

Full Retirement Age (FRA) – This is the age that the SSA considers you reaching full retirement age, which is the age when you can collect 100% of your SS retirement benefit (if you haven’t started collecting early, prior to your FRA). Your FRA ranges from age 65 to 67 and is based on your birth year. Anyone born prior to 1938 has an FRA of 65. Those born in 1960 or later have an FRA of 67. Those born 1938 or later, but before 1960, have an FRA somewhere between ages 65 and 67. Here is the chart to determine your FRA. One more thing, the FRA of a widow might be slightly different by one to four months from their regular FRA.

Primary Insurance Amount (PIA) – This is the monthly amount of SS retirement benefit earned by you if you were to start collecting your own SS retirement benefit at your FRA (age 65 to 67). Each spouse has their own PIA based on their own SS earnings record. This PIA is the amount used for ALL calculations related to spousal, survivor, early or delayed and young children benefits. Everything revolves around the PIA.

Delayed Retirement Credits (DRC) – If you delay the start of your own SS retirement benefit beyond your FRA, your benefit can increase 8% each year you delay, up to age 70 (those born prior to 1943 might have received a lower annual DRC rate; with the lowest rate at 5.5% per year). These DRCs are earned monthly, not annually. The 8% annual rate is actually earned at the rate of 8/12th of one-percent each month. One does not have to delay a full year before earning an 8% credit. If your FRA is age 67 and you delay the start of your benefit until age 67 years and 4 months, you earn 4 months’ worth of DRC (4 x 8/12th of one-percent equals a 2.33% credit). Delaying the start of your own SS benefit beyond your age 70 provides no additional DRCs. Earning DRCs results in a permanent increase of benefits (for the rest of your life!). For many (not all) people delaying the start of their SS is a smart move. Later on, we will go into detail on when delaying the start of SS benefits makes sense and certain situations when delaying may not make sense.

Now, we’ll look at the SS timeline and key ages as they relate to eligibility of retirement, spousal and survivor benefits and how those benefits can change based on when they are started. We’ll try to boil all the SS rules down to a simple flowchart that may help get you headed in the right direction regarding who gets what benefits after a spouse dies.

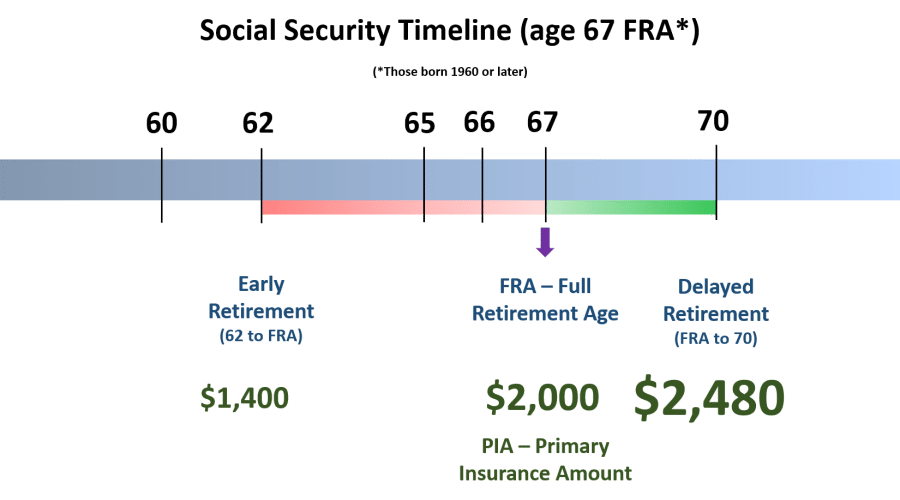

Social Security Timeline

The graphic below depicts the standard Social Security (SS) timeline from ages 60 to 70. For retired or nearly-retired couples, this 10-year timeline is where most of the SS decisions are made. For younger widows and those raising children, the timeline expands to include a broader range of younger ages. Each posted age on the timeline below represents a change in eligibility or amounts of various SS benefits. Let’s visit each age on the timeline to understand the impact of reaching that age:

Age 60 – Is the youngest age a widow (or widower) can collect SS survivor benefits, should their spouse pass away (survivor benefit is also known as the Widow’s Insurance Benefit). If the SS Administration considers the widow disabled, she may collect survivor benefits as early as age 50. At age 60, the widow is not yet eligible for her own retirement SS benefit, just the survivor benefit. Starting the survivor benefit at age 60 will result in a reduced benefit; typically 71.5% of the full survivor’s benefit. However, if the deceased spouse delayed benefits (past their FRA) or started them early (prior to their FRA), there are several complex factors to consider which will be detailed later on in this post. Remarriage and/or raising young children can also affect certain survivor benefits.

Age 62 – The earliest age that an eligible person can start their own SS retirement benefit or collect a spousal benefit. Collecting a spousal benefit may require your spouse to already have started or filed for their own SS retirement benefit.

Age 65 – The Full Retirement Age (FRA) for those born prior to 1938. Age 65 is also the age that most people are eligible to start Medicare Parts A and B (disabled individuals may qualify for Medicare prior to age 65). Previously, we discussed the fact that FRA is the point where an individual can collect 100% of their retirement benefit (this 100% amount is known as the Primary Insurance Amount or PIA) if they haven’t already started collecting it earlier.

Age 65 to 67 – For those born in 1938 or later, your FRA will range between ages 65 and 67, in two-month increments. If you were born after 1959 (so 1960 or later), your FRA is age 67. For everyone else (born 1938 through 1959) your FRA is somewhere between ages 65 and 67. Here’s the chart to determine your FRA. As a widow, your survivor’s FRA might be different than your retirement FRA by up to four months (take a look at the chart half way down the linked page).

Age 70 – This is the latest you can delay your own SS retirement benefit and earn Delayed Retirement Credits. Delaying the start of your own retirement benefit beyond age 70 earns no higher benefit. For the survivor benefit, delaying it beyond your FRA provides no larger benefit. Examples are provided later.

How do Social Security retirement benefits change if you or your spouse starts collection early or late compared to starting at FRA?

For many of the scenarios, it’s beneficial to understand how SS retirement benefits change when a person decides to start collecting on-time, early or late. The decision your spouse makes to start their SS retirement benefit early (prior to their FRA), on-time (at FRA), or delayed (after FRA and up to age 70), may impact how much in survivor benefits you receive as a widow.

In the timeline below, let’s say a husband was born in 1954, making him 60 in 2014. His wages over the past 35 years have earned him a SS retirement benefit of $2,000 per month if he starts his benefit at his Full Retirement Age, which is 66. This $2,000 is his Primary Insurance Amount (PIA) and is the reference amount used to calculate all other benefits for spouses, survivors, children, early and delayed benefits.

If the husband decides to take his own SS retirement benefit early, at age 62, he receives an amount less than $2,000 per month. Because his FRA is age 66 and he starts his benefit four years early, he would receive 25% less or $1,500 per month. If he starts benefits anywhere between age 62 and 66, the monthly amount would be between the $1,500 and $2,000 per month. Benefit adjustments, for starting early (prior to FRA) or delayed (past FRA) are calculated in monthly intervals, not annual intervals.

If the husband starts his retirement benefit 18 months prior to his FRA, his benefit will be reduced by 18 x 5/9% = 10% or $1,800 per month. If he starts 12 months early, the reduction is 12 x 5/9% = 6 2/3% or about $1,867 per month. If he starts 24 months early, the reduction is 24 x 5/9% = 13 1/3% or about $1733 per month. The monthly reduction fraction changes from 5/9% to 5/12% for those months he starts more than 36 months early. The first 36 months are still reduced by 5/9%. If he starts 48 months early at age 62, his total reduction is 25% (5/9% x 36 + 5/12% x 12 = 20% + 5% = 25%) or $1,500 per month. Aside from potential annual Cost of Living Adjustments (COLA), starting a retirement benefit early results in a permanent reduction over his lifetime.

Let’s say the husband works through his sixties and decides to delay the start of his SS retirement benefit until age 70. Every full 12 months he delays past age 66 earns him an 8% credit (Delayed Retirement Credit [DRC]) on top of his $2,000 per month. Since there are four years between age 66 and 70, the 8% per year credit produces a 32% increase in benefit above the PIA ($2,000/mo). In this case the age 70 benefit is $2,640 per month ($2,000 x 1.32). DRCs are offered at monthly intervals, not just full year delays. Each month one delays earns them an 8/12% (0.667%) increase in retirement benefit. Each 12 months of delay provides 12 x 8/12% = 8% increase.

The age 70 retirement benefit of $2,640/month is 76% higher than the age 62 retirement benefit of $1,500/month! That’s significant and needs to be considered when applying for benefits, especially when thinking about survivor benefits for your spouse.

What SS benefits Can I Collect After My Spouse Dies?

Social Security is complicated. Every person has 96 different months they can start collecting their own retirement benefit. The same person might also have spousal or survivor benefits to consider. Their spouse may have had a similar number of options. Combined, Social Security Solutions, Inc reports that a couple could have over 10,000 possible claiming options to consider! One’s search for the optimal SS claiming strategy might get even more complicated if Government pensions, excessive earnings prior to FRA, raising minor children, disability, remarriage, and ex-spouse benefits come into play.

With all those potential claiming options, is there an easy way to answer the question, what SS benefits can I collect after my spouse dies? Not exactly, but you can at least get headed in the right direction by considering a few rules of thumb. Run through the flowchart below to help you get pointed in the right direction*. Realize that a full analysis of your situation is probably required to get the most out of your eligible SS benefits. Discussion of the flowchart’s four possible outcomes is provided further down the post.

*This flowchart represents a very basic overview of SS claiming rules and does not reflect all the detailed quirks and exceptions of the SS system and your situation. There are many caveats which are not depicted in this simple flowchart. For example, if your ex-spouse dies and you were married to them for at least 10 years and are currently not married, you may qualify for survivor benefits based on their SS earnings record.

Another example of exceptions is working credits. The flowchart assumes the deceased spouse earned enough SS working credits to meet SS eligibility requirements. Fully Insured status normally requires 40 working credits (earned at a rate of 4 work credits per year) for retirement benefits but the number of working credits is less for younger workers. Also, there is a special rule that allows the SSA to pay survivor benefits to the deceased’s children, and spouse while she is caring for the deceased’s children, with as little as 6 work credits (see bottom of linked page) if earned in the three years just prior to death. There are many exceptions.

It’s always best to find out your benefit claiming options from your local SS representative and then, before signing up for benefits, get an in-depth Social Security claiming strategy analysis from a qualified advisor.

General Flowchart Results and What They Mean to You

The flowchart is based on the recent death of your current spouse (no remarriage). Work your way through the above flowchart to reach one of the four results (panels #4, 5, 6 or 7) and then find the appropriate paragraph below for additional information that might help your understanding. Keep reading to read detailed examples that represent each of the four flowchart results will be discussed.

Flowchart panel #4. You may be eligible for survivor benefits if they are higher than your own; analysis is required.

In this scenario, you have already started your own SS retirement benefit, or you may be collecting a SS spousal benefit based on your spouse’s SS earnings record, and your spouse was not collecting a benefit at the time of their death. If you are newly widowed and age 60 or older, you may qualify for a survivor benefit (if you haven’t remarried prior to your age 60). Your spouse, in this scenario, may not have collected their own retirement benefit because they were too young to collect, or maybe they decided to delay their own retirement benefit and let it grow (a strategy called File and Suspend, which was eliminated in Nov 2015 for most married couples). This scenario requires determination of available SS retirement and survivor benefits followed by the proper analysis to find the optimal claiming strategy. Below, we will cover several scenarios meeting the condition of panel #4.

Flowchart panel #5. Depending on benefit start dates, you may be eligible for a benefit close to the highest eligible benefit; analysis is required. Both spouses have started SS benefits in this situation. One may have started their own retirement benefit and the other a spousal benefit. Or perhaps both are collecting their own retirement benefit. If one or both started benefits early (prior to their own FRA), the early start date(s) could affect the benefits available to the widow. The key is to understand the start date and type of each spouse’s benefit so that an optimal claiming strategy is found for the widow.

Flowchart panel #6. Most likely no SS benefits are currently available but contact the SSA to be sure.

If you are under age 60, you most likely are not eligible for SS survivor benefits unless you are disabled or have one or more children that have not yet reached age 16. Your children may be eligible for their own children’s benefit (which is one type of survivor benefit) in certain circumstances. A widow can collect survivor benefits as early as age 60 (age 50 if disabled). Whether it’s wise to collect survivor benefits at age 60 is explained in more detail below.

Flowchart panel #7. You and/or your children under age 19 may be eligible for SS survivor’s benefits; analysis is required.

If you are newly widowed and age 60 or older, you may qualify for a survivor benefit assuming you haven’t remarried prior to your age 60. If you are disabled and at least 50 years of age, you may qualify for a survivor benefit. Lastly, if you are newly widowed and raising the deceased’s children who are unmarried and under age 16, you and each child may each be eligible for SS survivor benefits, up to the Family Maximum. Once the youngest child reaches age 16, then you no longer receive SS survivor benefits as the parent (unless you meet other requirements such as age 50 or 60 criteria discussed earlier in this paragraph). A child’s survivor benefit can continue until they reach age 19 and 2 months (if attending school) or graduate from high school, whichever occurs first. Children disabled prior to age 22 at the time of their parent’s death may be eligible for their own disability benefit and/or a children’s benefit, which may continue indefinitely.

Social Security Scenarios to Consider Depending on Age

This section applies all those SS basics to many different scenarios including age differences and similar versus different benefit amounts. To gain insight into claiming strategies as they relate to your situation, find the example or examples below that are closest to your situation to gain a better understanding of your situation. Armed with this knowledge, you are better prepared to know what benefits you might be eligible for and what questions to ask of a SS representative when you meet with them.

NOTE: The scenarios described here are educational in nature and may not represent your exact situation. Please do not use these educational scenarios as advice or guidance as to what decisions you should make regarding your SS benefits. It is always recommended that you consult with the Social Security Administration (SSA) to learn of all available claiming options and then consider these options carefully.

Both Spouses are Over Age 70

Generally, both spouses should be collecting SS benefits if they are age 70 or older. Both might be collecting their own benefit or one might be collecting a spousal benefit if it is higher than their own SS benefit. Every now and then an individual is over age 70 and hasn’t applied to collect an eligible SS benefit! The SSA does check for these situations but sometimes a person falls through the cracks. Let’s look at a few examples when both spouses are over age 70 and one of them passes away.

Jack and Kate are past age 70 and both are collecting SS benefits. At Jack’s death, the surviving spouse, Kate, will receive an amount equal to the highest benefit received. If Jack was receiving his own monthly retirement benefit of $2,000 and Kate is receiving her own or a spousal monthly benefit of $1,000, upon Jack’s death, Kate will receive the higher amount ($2,000).

Reversing the amounts, if Kate is the one collecting $2,000 per month and Jack is collecting $1,000 per month, upon Jack’s death, Kate will not collect any more than $2,000 per month. Losing $1,000 a month in benefits can be an unwanted surprise to a surviving spouse, especially if savings or other sources of income are insufficient.

If both Jack and Kate were high wage earners and each is collecting $2,000 per month, that’s $4,000 per month. Losing $2,000 a month of the $4,000 is a 50% drop; a shock to the system for most people, especially if SS income is the major source of income for the couple. Most people realize that living expenses for a widow are not cut in half after the death of their spouse. Poverty, unfortunately, is a reality for many low-income widows.

If Kate was previously married for more than 10 years, and her ex-spouse is also deceased, Kate might be eligible for survivor benefits not only from her deceased spouse but also from her deceased ex-spouse. If the deceased ex-spouse’s own retirement benefit exceeded $2,000, which is more than Jack’s benefit, Kate might be able to claim that higher benefit from her ex-spouse’s SS earnings record. The lesson here is to check with the SSA regarding all eligible SS benefits, including those from ex-spouses.

One or Both Spouses Started Collecting SS Benefits Between FRA and Age 70

If you and/or your spouse started collecting SS benefits between FRA and age 70 and you are now older than 70, please read the section above titled Both Spouses are Over Age 70.

In this situation, at least one spouse waited to start collecting their SS benefit between their own FRA and age 70. The second spouse is either collecting their own SS benefit or delaying their own benefit while possibly collecting a spousal benefit.

As you know, waiting until FRA to collect your own retirement benefit allows you to collect 100% of your full retirement age amount known as your Primary Insurance Amount (PIA). Delaying the start past FRA allows you to collect Delayed Retirement Credits (DRCs) at the rate of 8% per year, up to age 70. Certain exceptions such as the Windfall Elimination Provision (WEP) and the Government Pension Offset (GPO) may affect one’s ability to collect full benefits at FRA; both are covered below if you keep reading.

Jack is age 68 and started collecting his own SS retirement benefit of $1,800 per month at age 66 (his FRA). Kate is 67 (her FRA is 66) and is delaying her own retirement benefit (PIA = $1,200) until her age 70 to collect $1,584 per month. Her own benefit, even with Delayed Retirement Credits (DRCs), will not grow bigger than Jack’s $1,800 benefit, so upon Jack’s death, Kate will file for and collect $1,800 per month. Because Kate is past her FRA, there is no advantage to her waiting to claim her survivor benefit. If Kate was between 60 and 66 when Jack died, there might be an advantage for her to wait until her FRA to collect a survivor benefit (see example further down this post).

Tweaking it a bit, let’s assume Jack waited to start his SS retirement benefit until age 68, thereby accumulating two years of DRCs at 8% per year for a total benefit of $2,088 ($1,800 x 116%). At Jack’s death, Kate, age 67, will collect $2,088 per month in survivor benefits. If Kate waits two years, until Jack would have reached age 70, she would not collect any more in survivor benefits, just the $2,088 (plus inflation).

Let’s reverse the initial scenario with Kate collecting $1,800 per month in retirement benefit and Jack delaying his benefit (PIA=$1,200). At Jack’s passing, Kate would continue receiving her $1,800 per month. The survivor benefit, if delayed any amount of time, does not grow larger than her $1,800, so survivor benefits would not exceed Kate’s current benefit.

One or Both Spouses Started Collecting SS Benefits Between Age 62 and FRA

If you and/or your spouse started collecting SS benefits between age 62 and FRA and you are now older than 70, please read the earlier section titled Both Spouses are Over Age 70.

When one or both spouses start collecting a retirement benefit prior to their FRA, their retirement benefit is reduced below their PIA and stays reduced for the rest of their lives, except for inflation adjustments. They do not accumulate any DRCs once they pass their FRA up to age 70, because they’ve already started their own benefit early.

If their FRA is age 66 and they start collecting their own retirement benefit at age 62 (four years early), they receive 75% of their Full Retirement Age (FRA) benefit. If their FRA is age 67 and they start collecting at age 62 (five years early), they receive 70% of their FRA benefit.

Let’s assume Jack is 64 and Kate is 62, FRA is 66 for both and each started collecting their own retirement benefit at their respective age 62; Jack received $1,350 (75% x $1,800) and Kate $750 (75% x $1,000) per month. Since each started collecting four years early, their retirement benefits were reduced 25%. Jack dies at age 64 and Kate is still 62. If Kate continues her own retirement benefit of $750 until she reaches her FRA, she can collect the higher of two amounts: 82.5% of Jack’s PIA (82.5% x $1,800 = $1,485) or the $1,350 he was receiving. The higher amount is $1,485 and because it is also higher than her $750, she will collect $1,485 per month. Notice that this survivor benefit ($1,485) is higher than what either of them was collecting individually ($1,350 and $750).

A note of interest is that Kate’s survivor benefit does not get reduced because she started her own retirement benefit early (prior to her FRA). The SSA site states “In many cases, a widow or widower can begin receiving one benefit at a reduced rate and then, at full retirement age, switch to the other benefit at an unreduced rate.”

If Kate decides to file for survivor benefits prior to her FRA, three specific amounts are calculated, arranged from low to high and compared to a table in the POMS. The name sequence matching the table indicates which of the three amounts Kate will receive. In this example let’s assume Kate applies for survivor benefits at age 62, the three amounts are 82.5% of Jack’s PIA (82.5% x $1,800 = $1,485), the amount Jack received ($1,350), and an amount proportional to when Kate starts the benefit between age 60 and 66 (in this case, for an age 62 start date it would be $1,800 x [28.5% x 24 / 72 + 71.5%] = $1,800 x 81.0% = $1,458). The three amounts are then ranked low to high: $1,350 (Reduced Insurance Benefit), $1,458 (Reduced Widow’s Insurance Benefit) and $1,485 (82.5% of PIA). This sequence matches the 5th sequence in the table which means this widow will receive the underlined amount (the middle amount), $1,458. This is a case, again, where Kate receives more than the amount she was collecting, and more than the amount Jack was collecting. It may benefit Kate to delay collecting her survivor benefit until later, but in this case, the increase might be negligible. Analysis is recommended to determine the best starting date to maximize her survivor benefit over her lifetime.

Surviving Spouse is between age 60 and 62

Kate is 60 and not yet eligible for her own SS retirement benefit or a spousal SS benefit (her FRA is 66 and PIA is $800). Jack is 67 and started his own retirement benefit of $1,800 per month one year earlier at age 66 (his FRA). Upon his death at age 67, Kate’s friends convince her to apply for survivor benefits now, at age 60. As a widow she is eligible to collect survivor benefits as early as age 60 (50 if disabled). Kate applies for and collects a reduced widow’s benefit equal to 71.5% of Jack’s $1,800 ($1,287 per month). In two years Kate turns 62 and she is now eligible to switch to her own retirement benefit, but only if it exceeds her survivor benefit. It does not and she continues to collect the survivor benefit. In fact, Kate’s own retirement benefit never grows larger than her survivor benefit, so she sticks with the larger survivor benefit for the rest of her life. Living to age 90, she will have collected about $470,000 in SS benefits (no adjustment for inflation).

Another strategy for Kate to consider is to take no survivor benefit at age 60 (she covers living expenses with retirement savings). When Kate turns 62 she starts collecting her own retirement benefit (75% of $800 = $600/month) and then at her FRA switches to a survivor benefit of $1,800 (Jack’s PIA). By age 90 she will have collected just over $540,000 (no inflation adjustment) in SS benefits which is about $70,000 more than the strategy recommended by her friends. If she lives five years longer to age 95, Kate will have collected nearly $100,000 more in lifetime SS benefits. Picking the optimal claiming strategy depends on a few factors including life expectancy. If Kate is in poor health, she may not expect to live to age 90, with age 95 being even more of a stretch, so starting benefits earlier may make more sense. Analysis is recommended.

Editors Note: This article was originally published as a 3 Part Series beginning in December of 2018. It has been updated and republished to make it easier to access.

DISCLAIMER: All written content on this site is for information and education purposes only and is not specific advice for your situation. Opinions expressed herein are solely those of Widowed Community, LLC and the Widowed Community Financial Blog, unless otherwise specifically cited. Material presented is believed to be from reliable sources. We do not endorse any 3rd party comments or posts (3rd parties are those readers of The Blog who choose to submit comments). All information or ideas provided should be discussed in detail with a qualified financial advisor, accountant or legal counsel prior to implementation. See our Terms of Use for additional details regarding legal disclaimers, privacy policy, permissions & reprints and comment policy. The FAQs page also contains some good information.

Jim Schwartz is a Scottsdale, AZ fee-only financial planner with an expertise and interest in financial planning and education for widows and widowers.

Recent Comments